Choose a bank account by matching fees, interest, access, and features to your goals-daily spending, emergency savings, or long-term growth.

Start with clarity: track income, list debts, build a small emergency fund, and set one savings goal. A simple checklist turns daily spending into deliberate financial decisions.

Build a budget around actual habits: track income, fixed bills, flexible spending, and savings goals, then review monthly so surprises don’t derail your plan.

Protect your online banking: use unique passwords, enable two-factor authentication, avoid public Wi-Fi, and review account alerts regularly for suspicious activity.

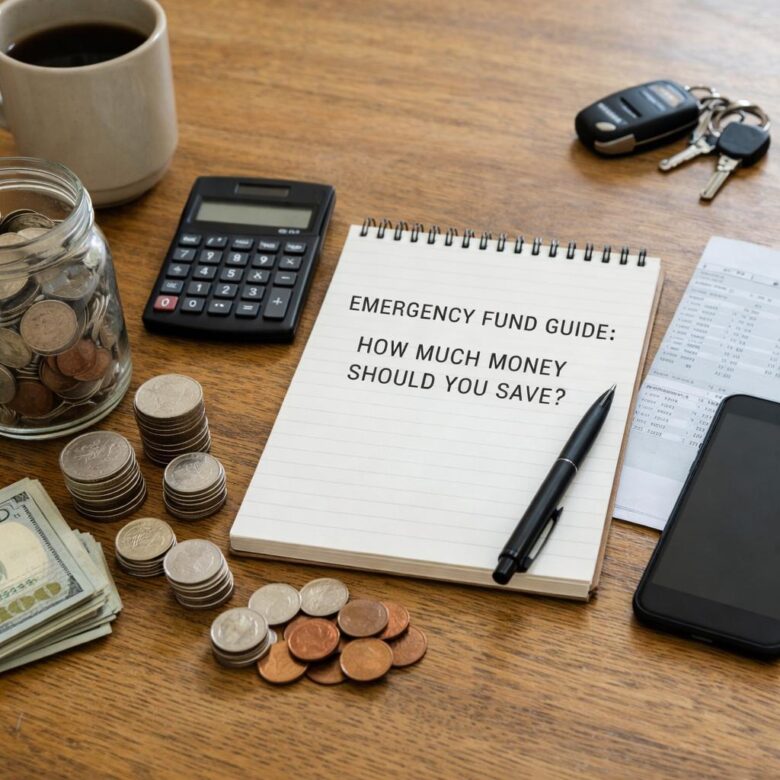

Emergency fund: Save 3-6 months of essential expenses in a liquid account. Start with $1,000, then adjust for income stability, dependents, and risk.

Insurance helps protect your finances from unexpected loss. Beginners should compare coverage, premiums, deductibles, exclusions, and claim steps before choosing a policy.

Annual review: Check dwelling limits, deductibles, liability coverage, valuables, discounts, and recent renovations to keep your home insurance aligned with current risks.

Common budgeting mistakes include underestimating variable costs, ignoring small purchases, and failing to adjust plans monthly-habits that quietly reduce your ability to save.

Compare financial products by focusing on total cost, risk, flexibility, and long-term value-not headline rates. Use the same criteria for each option to avoid confusion.

Life insurance protects beneficiaries after death, while health insurance helps cover medical costs during life. Knowing both clarifies financial planning.